Florida Insurance Rates Are Finally Dropping in 2026 — But Here's the Trade-Off Homeowners Need to Know

For years, Florida homeowners have been hit with some of the highest insurance premiums in the country. Every year, renewal letters arrived with bigger and bigger numbers. Many families had to make tough choices between keeping their coverage or paying other bills.

But last week, Governor Ron DeSantis announced some good news. Starting this spring, hundreds of thousands of Florida homeowners will see their insurance premiums go down. For many families, this is the relief they've been waiting for.

However, there's an important catch that most news stories aren't talking about. The same laws that made these rate drops possible also took away some of your rights as a policyholder. This means when your claim gets denied or underpaid, you have fewer ways to fight back.

Let's break down what this means for you.

The Good News: Rates Are Coming Down

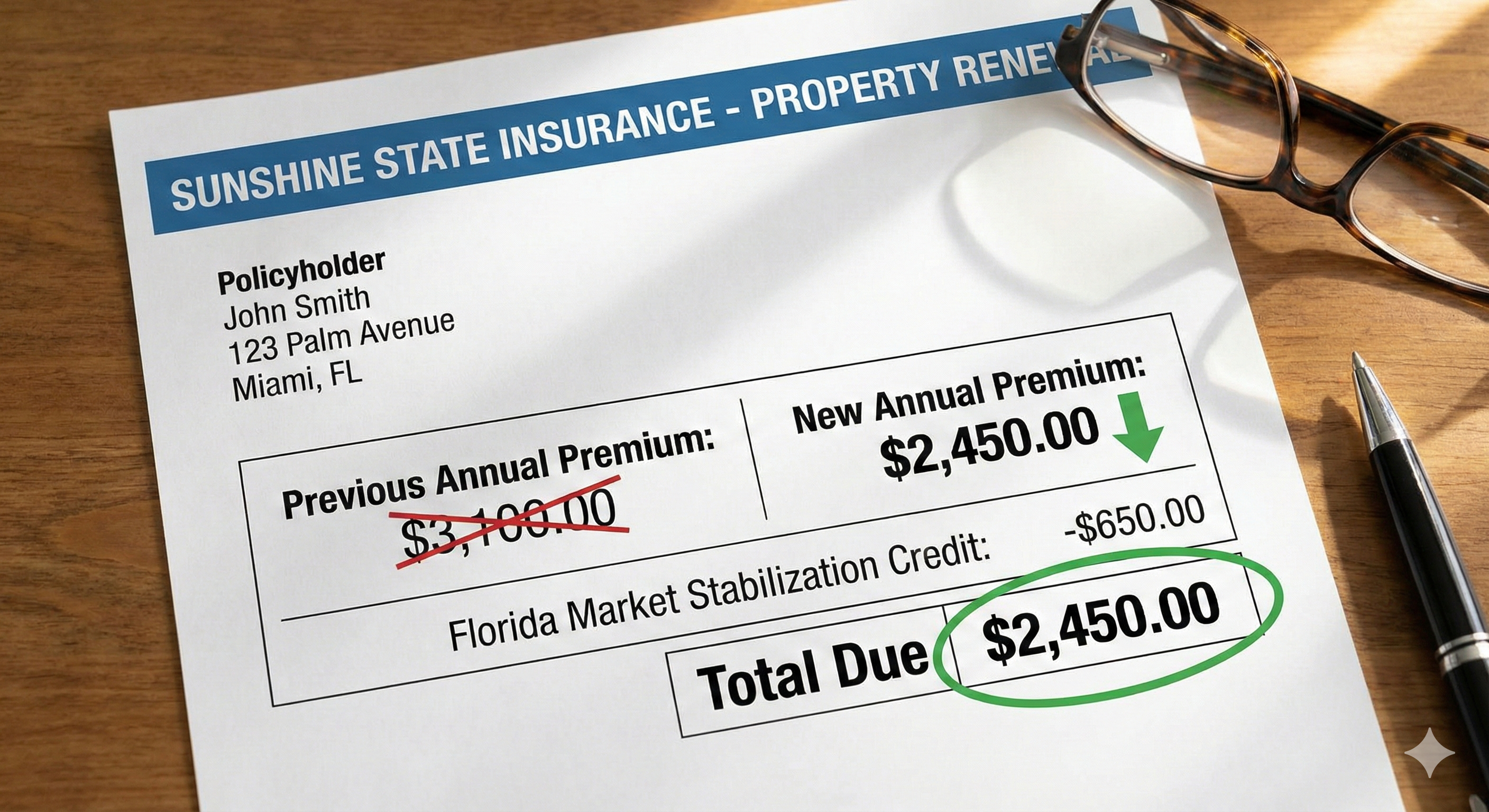

According to the Governor's office announcement, Citizens Property Insurance policyholders will see an average rate reduction of 8.7% starting in Spring 2026. More than 330,000 policyholders across all 67 Florida counties will get lower premiums.

Some areas will see even bigger savings:

- Miami-Dade County: About 42,000 homeowners will see an average reduction of 14%

- Broward County: About 27,000 homeowners will see an average reduction of 14.1%

- Palm Beach County: About 26,000 homeowners will see an average reduction of nearly 12%

- Monroe County: More than 1,000 homeowners will see an average reduction of 11.3%

It's not just Citizens policyholders who benefit. Many private insurance companies have also filed for rate decreases. State Farm filed for a 10% reduction. Florida Peninsula is proposing an 8.4% cut. Heritage, Security First, and others are following suit.

This is real progress. After years of double-digit increases, Florida's insurance market is finally stabilizing.

The Trade-Off: You Have Fewer Options When Claims Go Wrong

Here's the part that doesn't make the headlines.

Back in 2022 and 2023, Florida lawmakers passed major insurance reforms. These new laws were designed to reduce lawsuits against insurance companies. The idea was simple: fewer lawsuits means lower costs for insurers, which means lower premiums for you.

And it worked — sort of. Premiums are coming down. But those same laws also made it harder for homeowners to fight back when their claims are denied or underpaid.

What Changed?

One-Way Attorney Fees Are Gone

Before the reforms, if you sued your insurance company and won, they had to pay your attorney fees. This meant lawyers were willing to take your case even if you couldn't afford to pay upfront. The insurance company took the risk of paying legal costs if they were wrong.

Now, that's no longer the case. If you sue your insurance company, you might have to pay your own attorney — win or lose. This makes it much harder to find a lawyer willing to take your case.

Assignment of Benefits (AOB) Is Restricted

You also can't easily sign over your insurance benefits to a contractor anymore. This used to be one way homeowners could get repairs done without dealing with the insurance company directly. Now, this option is much more limited.

What This Means for Your Claim

With less threat of lawsuits, some insurance companies may feel more comfortable offering low settlements. They know it's harder for you to fight back now.

Think about it this way: If you're playing a game and there's no penalty for breaking the rules, some players might start bending them. The same thing can happen with insurance claims.

This doesn't mean all insurance companies will act in bad faith. Many are fair and honest. But the safety net that used to protect homeowners from bad behavior has gotten smaller.

Why Public Adjusters Matter More Than Ever

Here's the good news: you still have options.

A public adjuster can step in and advocate for you during the claims process — before things escalate to a lawsuit. We speak the same language as the insurance company's adjusters. We know what documentation they need. We understand how to read your policy and fight for every dollar you deserve.

Understanding the difference between public adjusters and insurance company adjusters is key. The insurance company's adjuster works for them. A public adjuster works for you.

Unlike hiring an attorney to sue after the fact, working with a public adjuster costs you nothing out of pocket until you get paid. We work on contingency — meaning we only get paid if we recover money for you.

Common Situations Where We Can Help

If any of these sound familiar, it might be time to call us:

-

Your claim was denied — Insurance companies deny claims for many reasons. Sometimes they're right. Often, they're not. We can review your denial and tell you if it's worth fighting. Learn about common denial reasons for fire claims — many of these apply to other claim types too.

-

Your settlement seems too low — Did the insurance company's adjuster spend 15 minutes on your roof and offer you a fraction of what repairs will actually cost? That happens more than you'd think.

-

You're overwhelmed by the process — Filing a claim involves paperwork, phone calls, inspections, and deadlines. Most people have never done this before. We do it every day.

-

You have roof damage — The 25 percent rule for roofs is one of the most misunderstood parts of Florida insurance. Insurance companies often use it to underpay claims. We can help you understand your rights.

The Bottom Line

Lower insurance rates are great news for Florida homeowners. It's been a long time coming.

But don't let the celebrations make you forget: when something goes wrong with your claim, you have fewer legal options than you did a few years ago. The reforms that brought rates down also shifted power toward insurance companies.

That's why getting it right the first time matters more than ever. Having an experienced advocate on your side during the claims process — not after — can make all the difference.

Get a Free Claim Assessment

If you've had a claim denied or underpaid, or if you're just not sure whether your insurance company is treating you fairly, we're here to help.

At NeJame Claims Adjusting, we offer free claim assessments. We'll review your situation, explain your options, and tell you honestly whether we think we can help.

Call us at (407) 637-1000 or contact us online to schedule your free consultation.

NeJame Claims Adjusting is a licensed public adjusting firm serving homeowners throughout Central Florida. We work exclusively for policyholders — never for insurance companies.