Florida Property Insurance in 2025: What Homeowners Need to Know About Changes to Claims and Coverage

For years, Florida homeowners have watched their insurance bills climb while their policies shrink. Storms, lawsuits and company failures have shaken confidence in the state’s insurance system. The Legislature’s sweeping reforms in 2022 and 2023 have begun to stabilize the market, but 2025 introduced its own mix of new laws, market trends and debates. As a public adjusting firm, NeJame Claims Adjusting wants you to understand how these developments affect your ability to file a claim, get fair payment and keep your coverage. We’ve written this guide at about an eighth‑grade reading level, so it’s easy to follow even if you’re not an insurance expert.

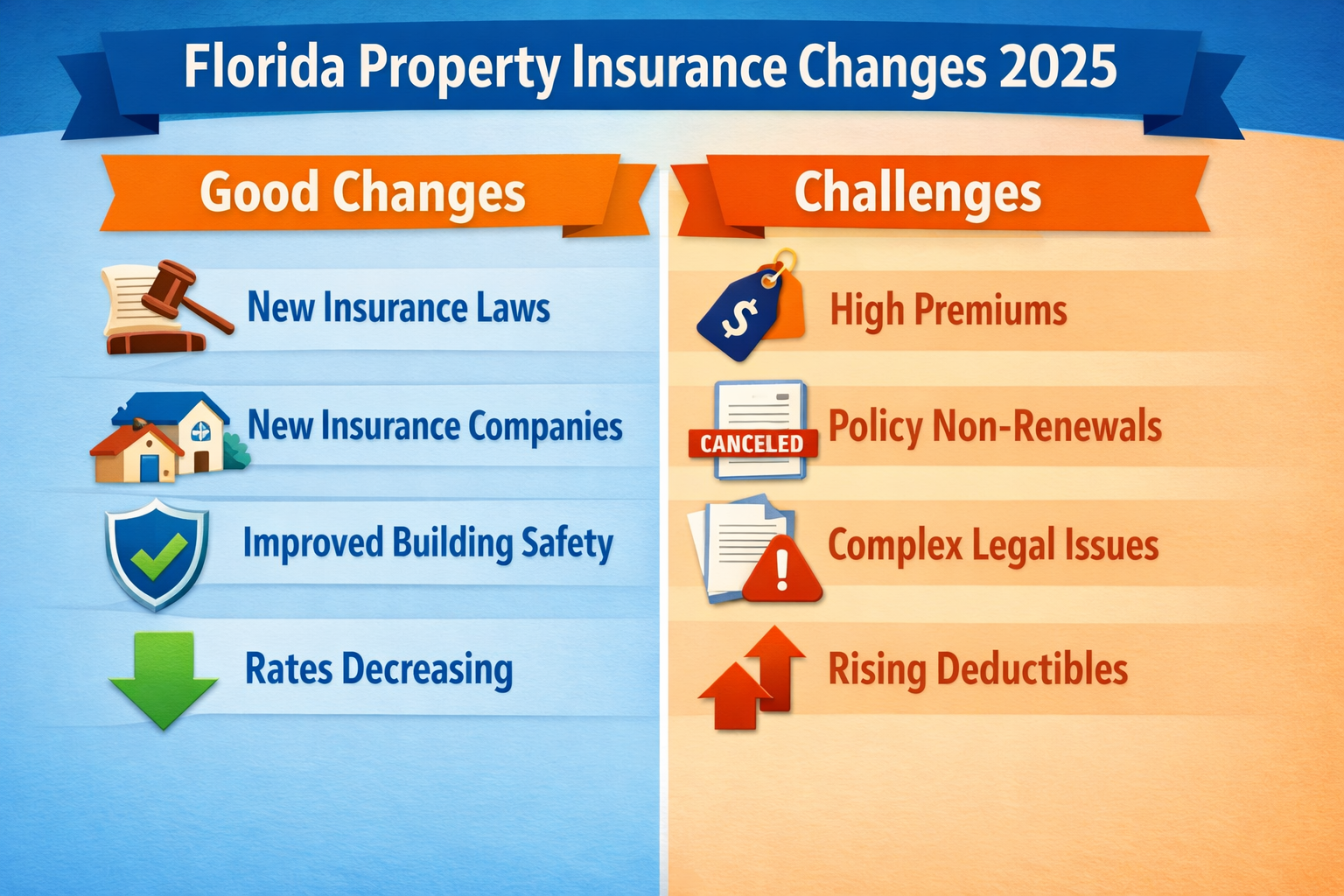

We’ll start with an overview of the market and then break down the new laws. We’ll point out the positive trends—rate reductions and new carriers—as well as the challenges that remain, such as complex policy language and high deductibles. Finally, we’ll offer practical tips for preparing for storms, filing claims and protecting your rights.

A Market in Transition

By late 2023, Florida’s property insurance market was in crisis. Premiums had doubled over just a few years, and a half‑dozen insurers had become insolvent. Lawsuits flooded the courts, many based on assignment of benefits agreements and one‑way attorney fee rules that made it profitable to sue insurers, even on small claims. To stabilize the system, lawmakers enacted a set of reforms. They banned most assignments of benefits, eliminated one‑way attorney fees in first‑party lawsuits, shortened the deadline to report a claim to one year and created a state reinsurance program. They also overhauled Citizens Property Insurance, raising eligibility thresholds and requiring policyholders to buy flood insurance.

Those reforms began to work. Lawsuits dropped by nearly a quarter, and about a dozen new insurers entered the market. By early 2025, nearly half a million policies had migrated from Citizens back to private carriers. Average rate increases fell sharply, and some companies even cut their rates. However, these improvements came with trade‑offs. Homeowners now shoulder more litigation risk, must meet tighter deadlines and often face higher deductibles. Understanding the new rules is essential to getting the coverage you pay for.

Laws Enacted in 2025 and What They Mean for Claims

SB 948 – Flood Disclosure

This law requires landlords and sellers to tell tenants and buyers if a property has flooded before or is in a flood zone. If you rent a home and your landlord didn’t disclose past flood damage, you can terminate your lease after a flood loss. When you buy property, the flood disclosure must be separate from other paperwork, which helps ensure you see it. The goal is to encourage informed decisions and push more homeowners to buy flood insurance, since standard property policies do not cover flood damage.

HB 393 – My Safe Florida Condo Pilot Program

Condo residents gained a new resource in 2025. HB 393 created a pilot program that extends the existing My Safe Florida Home grants to condominium associations. To qualify, a condo association must undergo a milestone structural inspection, fund a structural integrity reserve and obtain approval from 75% of unit owners. Once eligible, the association may receive matching funds to install impact‑resistant windows, doors and stronger roof attachments. These upgrades make buildings safer and reduce claims after a storm. As a unit owner, you should ask your board whether it plans to apply for these grants. Better mitigation means lower risk and may lead to lower assessments after a disaster.

HB 715 – Roofing Services

Your roof is the first line of defense against wind and rain. HB 715 allows licensed roofing contractors to inspect and strengthen roof‑to‑wall connections without having to hold a general contractor license. Roof‑to‑wall connections include metal straps or clips that attach roof rafters to wall studs. Strengthening these ties can prevent the roof from lifting off during a hurricane. The law also gives homeowners more time to cancel roofing contracts signed under emergency conditions and requires clear notices of your rights. For claimants, this matters because insurers are more willing to renew policies and pay promptly when a roof is up to code. Poor connections, on the other hand, can lead to denied or reduced claims.

HB 913 – Condominium and Cooperative Associations

This law increased oversight of condo and cooperative boards. It requires associations to purchase replacement‑value insurance for the common elements and to update those policies at least every three years. Associations must maintain detailed records on their websites, fund reserves for structural repairs and undergo regular inspections. Board members must take education courses. For condo unit owners, these requirements mean better transparency and fewer surprises when it comes to special assessments or insufficient insurance. If your association fails to carry adequate coverage and a disaster strikes, your claims against its policy might fall short. Ask your board for proof of coverage and a copy of the latest inspection report.

HB 1549 – Surplus Lines Insurance

Florida’s admitted insurers must file rates and policy forms with the state Office of Insurance Regulation (OIR), but surplus lines insurers do not. They step in when admitted companies won’t write a policy—often because the property is too risky or located in a high‑exposure area. HB 1549 repealed the rule that required agents to seek quotes from three admitted insurers before turning to a surplus lines carrier. The law also requires agents to give you a disclosure stating that surplus lines policies are not subject to OIR rate or form approval. This change gives homeowners more options, but it shifts more responsibility onto the policyholder. Surplus lines policies can have higher rates, unique deductibles and fewer consumer protections. When shopping for insurance, ask your agent whether you’re being placed with a surplus lines carrier and read the policy carefully.

HB 655 – Pet Insurance (Effective Jan 1, 2026)

While not directly related to homeowner claims, HB 655 is worth mentioning. The law classifies pet insurance as a form of property insurance, not health insurance, and sets consumer protections. It prohibits marketers from disguising wellness plans as insurance, limits waiting periods to 30 days, requires clear disclosure of pre‑existing condition exclusions and gives buyers a 30‑day free‑look period. Agents who sell pet insurance must receive special training. The law takes effect in 2026. While this doesn’t affect your home policy, it reflects a trend toward more detailed regulation of insurance products.

Market Trends: Rates, Carriers and Citizens

Slowing Rate Growth and Emerging Discounts

One of the best pieces of news for homeowners is that rate growth nearly stopped in 2025. Between August and September, the average all‑perils premium for owner‑occupied homes increased by only $1 statewide. Premiums rose 1.5% in the first nine months of the year, the smallest rise since the state began monthly reporting. Thirty‑eight insurers reported reductions in September, and several announced larger cuts. Security First Insurance reduced rates on its standard HO3 policy by 8%—its second consecutive year of cuts—and provided discounts up to 20% for newly built homes. Other companies filed for modest reductions as well. The result is that many homeowners renewed their policies at the same price or slightly lower.

New Carriers and Depopulating Citizens

Lower litigation risk and better oversight have attracted more companies back to Florida. Industry reports cite 11 to 14 new insurers entering the market since 2022. Many of these carriers participate in the Citizens depopulation program, meaning they take over policies from Citizens mid‑term without raising the premium until renewal. Patriot Select is one example; it reduced premiums for its takeout customers by more than 11%. In total, about 477,000 policies moved from Citizens to private companies by early 2025. This shift is significant because private carriers generally offer broader coverage and more flexible options than Citizens, which is intended as a last resort.

Average Premiums Remain High

Despite the slowdown, premiums remain costly. The average statewide premium of $3,748 in September is 34% higher than after the first set of reforms in 2022. Many policies now carry hurricane deductibles of 2% or 5% of the insured value. Construction inflation also plays a role: labor and materials cost more than they did a few years ago. Some regions, especially coastal counties, see even higher premiums. While the overall trend is improving, homeowners should budget carefully for insurance.

Continued Non‑Renewals and Tight Underwriting

Even with new carriers, insurers are still selective. They may refuse to renew if your roof is older than 15 years, if you have open claims or if your property is in a high‑risk flood zone. Proposed legislation in 2025 sought to prohibit non‑renewals or cancellations on homes damaged by hurricanes until repairs were completed, but those bills did not become law. Insurers therefore retain broad discretion. To keep your coverage, maintain your home’s condition, document repairs and respond quickly to any requests from your insurer.

Citizens: Lower Rates but More Requirements

Citizens has long been the insurer of last resort. Its rates are generally lower than private market rates, and for 2025 the company’s board even filed for a 2.6% average rate decrease for personal homeowners. However, Citizens policies come with stricter rules. The law now requires Citizens policyholders to buy flood insurance if their home’s replacement value exceeds $500,000 in 2025. That threshold drops to $400,000 in 2026 and will apply to all Citizens policies by 2027. Citizens also automatically transfers policies to private insurers if those insurers offer a renewal rate within 20% of the Citizens rate. If you’re covered by Citizens, be sure to watch for takeout offers and weigh the benefits and costs.

Proposed Bills That Didn’t Pass

Not all proposed changes became law. The most controversial bills in 2025 were HB 1551 and SB 426, which sought to revive attorney fee shifting in property insurance lawsuits. Under current law, each party pays its own legal fees unless they beat a formal settlement offer. The new proposals would have made the losing party—often the insurer—pay the other side’s attorney fees. Supporters argued that homeowners needed this to hold insurers accountable; opponents warned it would encourage frivolous suits and raise premiums. SB 554 proposed sliding‑scale attorney fees, mandatory mediation and strict timelines for claim handling. Other bills aimed to cap rate increases, create an administrative tribunal for claims disputes, or require insurers to give 45 days’ notice before any cancellation. These bills did not pass, but they signal an ongoing debate. Homeowners should stay informed because similar proposals may return in 2026.

How to File a Claim Successfully in 2025

Filing a property insurance claim can feel daunting. Changes in the law and tighter deadlines make it even more important to do things right. Here are steps to help ensure your claim is handled fairly:

-

Report Damage Quickly: Under current law, you have one year from the date of loss to file a new or reopened claim and 18 months for a supplemental claim. Waiting too long could bar your claim.

-

Document Everything: Take clear photos and videos of all damage. Keep receipts for emergency repairs, like tarps or temporary lodging. If water got inside, document the source and any mitigation measures you took, such as running dehumidifiers.

-

Don’t Sign Away Your Rights: Florida largely banned assignment of benefits. Avoid signing contracts that give a contractor the right to deal directly with your insurer unless you fully understand the consequences. If you hire a contractor for repairs, make sure the contract includes a cancellation period and does not assign benefits.

-

Know Your Deductibles: Check your policy to see if a hurricane deductible applies. If your home is damaged by a named storm, you must meet this higher deductible before coverage begins. For non‑hurricane claims, the standard deductible applies.

-

Communicate in Writing: Whenever possible, communicate with your insurer or adjuster in writing. Ask for confirmation when you submit documents. HB 1047, a bill considered but not passed in 2025, would have required adjusters to provide certain notices in writing, but it’s still a good practice. Written communication creates a paper trail if disputes arise.

-

Consider Pre‑Suit Mediation: If you disagree with your insurer’s offer, you may request mediation through the Department of Financial Services. Mediation is voluntary for most claims, but proposed bills in 2025 would have made it mandatory. Even without those bills, mediation can help resolve disputes without litigation.

-

Hire a Public Adjuster When Needed: A public adjuster represents you, not the insurance company. At NeJame Claims Adjusting, we inspect the damage, estimate the cost of repairs and handle communications with your insurer. We charge a percentage of the claim, which is capped by law. A public adjuster can be especially useful if your claim is complex or if the insurer’s initial estimate seems low.

-

Consult an Attorney for Legal Questions: If you believe your insurer is acting in bad faith or if a dispute cannot be resolved through mediation, consult an attorney who specializes in property insurance. Because attorney fees are no longer automatically recovered, attorneys may be selective in taking cases. Make sure you understand the potential costs.

Staying Prepared and Minimizing Losses

The best way to manage claims is to prevent damage in the first place. Here are steps you can take:

-

Wind Mitigation Upgrades: Reinforce roof‑to‑wall connections, install a secondary water barrier, and secure your roof deck. Impact‑resistant windows, doors and shutters can keep wind and debris out. These upgrades often lead to insurance discounts.

-

Regular Maintenance: Clean gutters, trim trees and fix minor roof issues promptly. Water intrusion from neglected maintenance may not be covered.

-

Flood Protection: Even if you’re not in a high‑risk zone, consider purchasing flood insurance. Elevate important systems like HVAC units and install backflow valves. When possible, landscape your yard to direct water away from the foundation.

-

Emergency Plan: Create a hurricane kit with supplies, know your evacuation zone and practice securing your property. Store important documents, including your insurance policy and inventory of belongings, in a waterproof container or cloud storage.

-

Condo Engagement: If you live in a condo, attend association meetings, review budgets and reserve studies and vote for board members who prioritize maintenance and transparency. Encourage your association to apply for My Safe Florida Condo grants.

Looking Ahead

Florida’s property insurance landscape is slowly improving. Rate increases have nearly leveled off, and some insurers are cutting premiums. New laws passed in 2025—like those covering flood disclosure, condo safety and roofing practices—provide more transparency and encourage stronger construction. At the same time, the market is still challenging: premiums remain high, non‑renewals are common and the legal environment remains uncertain. Bills proposing to restore attorney fee shifting and other litigation incentives may resurface in 2026.

As a homeowner, the best approach is to stay informed, maintain your property and keep good records. Understand your policy, know your deductibles and act quickly after a loss. At NeJame Claims Adjusting, we stay on top of legislative changes and market trends so that we can advocate for you when it matters most. If you need help navigating a claim or have questions about your coverage, reach out to us. We’re here to make sure you get the full benefits of your insurance and to guide you through the complexities of Florida’s insurance system.