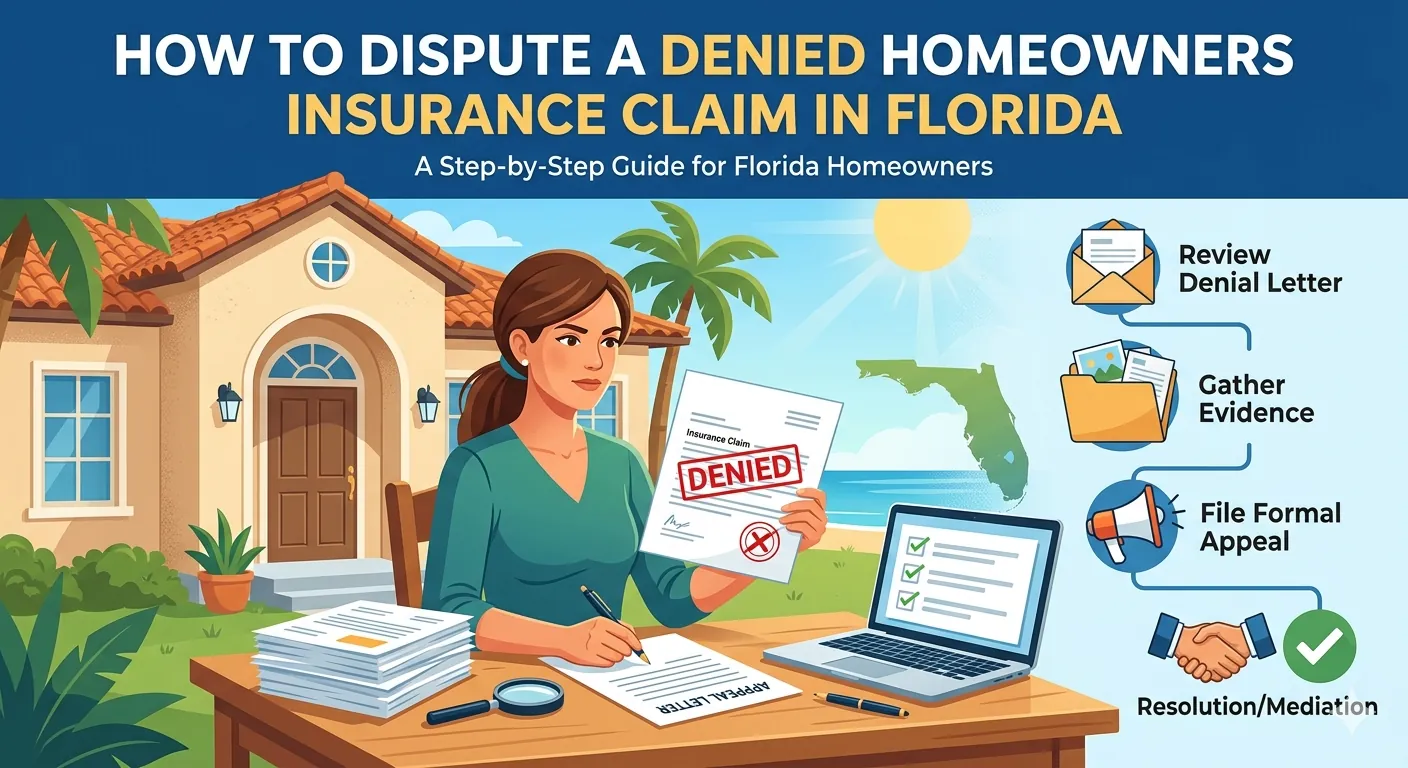

How to Dispute a Denied Homeowners Insurance Claim in Florida

If your Florida homeowners insurance claim was denied, you have several options to fight back: request a written explanation and review it against your actual policy language, hire a public adjuster to reopen the claim with proper documentation, request free state-administered mediation through the Florida Department of Financial Services, invoke the appraisal clause in your policy if the dispute is about the amount owed, or pursue litigation with an insurance attorney. The right path depends on why your claim was denied and whether the dispute is about coverage or valuation.

Getting a denial letter is frustrating, but it is not the final word on your claim. Florida law gives homeowners specific rights and multiple avenues to challenge an insurer's decision. This guide walks you through each option in the order you should typically consider them — starting with the steps you can take immediately and progressing to the more formal dispute resolution processes.

Step 1: Get the Denial in Writing and Understand Why

Florida's Homeowner Claims Bill of Rights, codified under Florida Statute §627.7142, requires your insurance company to provide a written explanation for any claim denial. That letter must identify the specific policy provisions the carrier is relying on to deny your claim.

Read the denial letter carefully and then read those specific provisions in your actual policy — not a summary, not a declarations page, but the full policy language. Insurance companies sometimes cite exclusions that don't actually apply to your situation, mischaracterize the cause of damage, or overlook coverage that exists elsewhere in the policy.

The most common denial reasons Central Florida homeowners encounter include the carrier claiming the damage is due to wear and tear or lack of maintenance rather than a covered peril, asserting the damage is pre-existing and not related to a recent event, classifying the damage as flood (excluded under standard policies) when it may have been caused by wind or a sudden plumbing failure, or determining the damage falls below your deductible. Some of these reasons are legitimate. Many are not — or at least deserve closer scrutiny. If you've received a denial and aren't sure whether it holds up, our post on common reasons insurance companies deny fire claims covers denial tactics that apply across claim types, not just fire losses.

Step 2: Document Everything You Have

Before you take any formal action, make sure your evidence is in order. Photograph and video all damage from multiple angles. Save any temporary repair receipts. Gather contractor estimates, weather reports from the date of loss, and any correspondence with your carrier. If the insurance company's adjuster inspected your property, request a copy of their report and estimate — you're entitled to it.

Strong documentation is the foundation of every successful dispute. Carriers respond to evidence, not emotion. The more thoroughly you've captured the damage and its cause, the stronger your position will be at every stage of the dispute process.

Step 3: Hire a Public Adjuster to Reopen the Claim

For most denied or underpaid claims, this is the most effective next step before escalating to formal dispute resolution. A licensed public adjuster works exclusively for you — not the insurance company — and is trained to review policy language, inspect damage, prepare detailed estimates, and negotiate directly with your carrier.

A public adjuster can often identify what went wrong with the initial claim: damage that was missed during the carrier's inspection, policy language that was misapplied, or documentation gaps that led to the denial. They can then reopen the claim or submit a supplement with the evidence needed to get a different result.

At NeJame Claims Adjusting, our founder worked as a carrier-side staff adjuster before becoming a licensed public adjuster and a licensed general contractor. That combination means we understand how carriers evaluate claims internally, we know what documentation they respond to, and we can identify construction-related damage that a desk adjuster or a rushed field inspection might miss. If you're weighing whether professional help makes sense for your situation, our guide on whether to hire a public adjuster or handle your claim yourself can help you decide.

Public adjuster fees in Florida are regulated by statute: up to 20% of the settlement for standard claims, and up to 10% for claims related to a Governor-declared state of emergency. The fee is contingency-based, meaning you pay nothing unless the adjuster successfully recovers money for you.

Step 4: Request State Mediation Through the Florida DFS

If direct negotiation with the carrier — whether on your own or through a public adjuster — doesn't resolve the dispute, Florida offers a free, state-administered mediation program through the Department of Financial Services.

Under Florida Statute §627.7015, homeowners with residential property claim disputes of $500 or more (after the deductible) can request mediation. This is a non-binding, informal process where you sit down with a representative from your insurance company and a certified neutral mediator. The mediator doesn't decide your claim — they facilitate a conversation aimed at reaching a settlement both sides can accept.

Here's what you need to know about the mediation process. You can request mediation online through the Florida DFS Consumer Assistance Portal or by calling the Division of Consumer Services. The insurance company pays the full cost of the mediation conference. Once a mediator is assigned, the conference must occur within 21 days. You can bring a public adjuster or attorney to represent you at the conference. If a settlement is reached, you have three business days to rescind the agreement, as long as you haven't cashed the settlement check.

Mediation is designed as a pre-appraisal and pre-litigation step. Many claims are resolved at this stage, especially when the homeowner or their public adjuster comes prepared with strong documentation and a clear estimate of the loss. The key advantage of mediation is that it puts your carrier's representative in a room (or on a call) where they have to engage with the merits of your claim directly — something that doesn't always happen during the standard claims process.

Step 5: Invoke the Appraisal Clause

If your dispute is about how much the insurance company owes you — not whether your claim is covered at all — the appraisal process may be your strongest option.

Most Florida homeowners policies contain an appraisal clause, typically found in the "Conditions" section of the policy. Under this clause, either you or the insurance company can demand an appraisal when there's a disagreement on the amount of loss. The process works like this: each side selects an independent appraiser, the two appraisers attempt to agree on the value of the loss, and if they can't agree, they select a neutral umpire whose decision is binding.

There are a few critical things to understand about appraisal. It only resolves disputes about the dollar amount of the loss — it cannot address coverage denials. If your carrier denied your claim entirely (saying the damage isn't covered), appraisal is not the right tool. Some carriers have removed the appraisal clause from their policies entirely, so check your policy language before assuming it's available. You pay for your own appraiser and split the cost of the umpire with the insurance company. The appraiser you choose matters enormously — this should be someone with deep knowledge of construction costs and insurance scoping, not a general real estate appraiser.

Florida Statute §627.7015 also requires that insurance companies offer mediation before demanding appraisal. If your carrier tries to push you into appraisal without first offering mediation, they may have waived their right to compel it.

Appraisal is particularly effective for roof damage claims where the carrier acknowledged coverage but offered an amount far below actual repair costs. For context on how common underpayment is in these situations, Orange Contracting and Roofing's post on why Florida roof insurance payouts fall short walks through the typical gap between what carriers approve and what repairs actually cost. Their post on what to do after a storm damages your roof is also worth reading if your denial involves storm damage.

Step 6: File a Complaint with the Florida DFS

Alongside any of the above steps, you can file a formal complaint with the Florida Department of Financial Services, Division of Consumer Services. While a complaint doesn't automatically reverse a denial, it creates an official record of the dispute and triggers a review by the state.

The DFS will contact your insurance company and request their response to your complaint. This alone sometimes prompts a re-examination of the claim. If the investigation reveals that the carrier violated Florida insurance regulations — such as failing to properly investigate, failing to provide required notices, or acting in bad faith — the DFS can refer the matter to the Office of Insurance Regulation for administrative action.

You can file a complaint online through the Florida DFS website or by calling the Division of Consumer Services.

Step 7: Consult an Insurance Attorney

If your claim has been denied based on a coverage dispute that can't be resolved through mediation or appraisal, or if you believe your insurance company has acted in bad faith, it may be time to involve a property insurance attorney.

An attorney can do things a public adjuster cannot: file a lawsuit, send a Civil Remedy Notice under Florida Statute §624.155 for bad faith, and pursue damages beyond your policy limits. Under Florida law, insurers must pay or deny your claim within 90 days of receiving your proof of loss. Failure to meet that deadline, among other conduct, can constitute bad faith.

The 2022 and 2023 legislative reforms changed the litigation landscape significantly. One-way attorney fees were eliminated, which means winning a lawsuit against your carrier no longer guarantees they'll pay your legal costs. This makes it more important than ever to exhaust pre-litigation options — particularly mediation and appraisal — before filing suit. Orange Contracting's review of the 2025 Florida insurance changes explains these reforms and their practical impact on homeowners.

That said, litigation remains a necessary and effective tool when carriers refuse to honor valid claims. Many insurance attorneys work on contingency, meaning you pay nothing unless they recover money for you.

Important Deadlines to Know

Florida law imposes strict deadlines on property insurance claims. Missing them can permanently bar your ability to recover, regardless of how valid your claim is.

You generally have two years from the date of loss to file a first-party property insurance claim. Supplemental claims must be submitted within 18 months of the date of loss. For breach of contract actions against your insurer, the statute of limitations is five years. These deadlines make it critical to act promptly — especially if your initial claim has been denied and you need time to pursue dispute resolution.

Frequently Asked Questions

Can I dispute my claim after I've already accepted a payment? Yes. Accepting a partial payment from your insurance company does not waive your right to dispute the amount. You can still hire a public adjuster, request mediation, or invoke appraisal to pursue the difference between what the carrier paid and what the repairs actually cost.

How much does it cost to dispute a denied claim? The DFS mediation program is free to homeowners — the insurance company pays the full cost. Public adjusters work on contingency (no recovery, no fee). Appraisal involves paying for your own appraiser and splitting the umpire's cost. Attorney fees are typically contingency-based as well.

What if my insurance company removed the appraisal clause from my policy? Some Florida carriers have done this. If your policy doesn't contain an appraisal clause, that dispute resolution path isn't available to you. Mediation and litigation remain your options. This is one reason it's important to read your full policy before you need to use it.

Should I hire a public adjuster or an attorney first? In most cases, starting with a public adjuster makes sense. They can often resolve the claim through the carrier's own process — through supplemental documentation, mediation, or appraisal — without the cost and delay of litigation. If the carrier refuses to pay fairly despite proper documentation and negotiation, the claim can then be escalated to an attorney. For a deeper look at this question, see our post on the differences between independent, staff, and public adjusters.

How long does the dispute process take? It depends on the path you take. Mediation typically occurs within 21 days of a mediator being assigned. Appraisal can take several weeks to a few months depending on complexity and umpire selection. Litigation can take anywhere from several months to over a year. Working with a public adjuster from the start often shortens the overall timeline by getting the documentation right the first time.

Don't Accept a Denial as the Final Answer

Insurance companies deny and underpay claims every day. In 2024, nearly half of all Florida residential property insurance claims were closed without payment. That statistic doesn't mean those claims were all invalid — it means the system is difficult to navigate without professional help and a clear understanding of your rights.

At NeJame Claims Adjusting, we help Central Florida homeowners challenge denied and underpaid claims every day. We offer free, no-obligation property inspections, and we only get paid when you get paid. If your claim has been denied and you're not sure where to start, contact us for an honest assessment of your options.

Tags: denied insurance claim Florida, dispute insurance claim, Florida homeowners insurance, public adjuster, insurance claim denied, underpaid claim, insurance mediation Florida, appraisal process, Central Florida, Orlando public adjuster, insurance claim dispute, property damage claim, NeJame Claims Adjusting, Homeowner Claims Bill of Rights, insurance bad faith Florida