Hurricane Season Starts Today: Is Your Florida Property and Insurance Claim Plan Ready?

Today marks the official start of hurricane season, and for Florida property owners, that should mean more than stocking up on bottled water and batteries.

Hurricane preparation is not just about protecting your family during the storm. It is also about protecting your home, your business, your documentation, and your ability to recover after the storm passes.

Every year, we speak with homeowners and business owners who did the right thing by preparing physically, but were not prepared for the insurance claim process that followed. They did not have good pre-loss photos. They had not reviewed their policy. They were unsure whether they had flood coverage. They did not know what to do when the insurance company sent an adjuster, requested documents, delayed payment, or issued a low estimate.

The best time to prepare for an insurance claim is before you ever have one.

At NeJame Claims Adjusting, we represent policyholders, not insurance companies. Our job is to help property owners understand, document, present, and pursue their claims when property damage occurs.

Hurricane Season Runs from June 1 Through November 30

The Atlantic hurricane season officially runs from June 1 through November 30. While not every season brings a direct hit to your area, Florida property owners know that one storm can be enough to cause serious damage.

Even a “quiet” season can still produce a storm that affects your roof, windows, siding, fencing, pool enclosure, interior ceilings, flooring, cabinets, or commercial property. A storm does not need to be a Category 5 hurricane to create a complicated insurance claim.

Wind-driven rain, flying debris, falling trees, roof uplift, broken tiles, lifted shingles, water intrusion, and power outages can all create damage that may not be obvious right away.

The National Oceanic and Atmospheric Administration’s hurricane preparedness resources remind property owners to understand their hurricane risk, prepare before storms arrive, and know what to do before, during, and after a storm.

That is why the start of hurricane season is the right time to take a serious look at your property and your insurance claim readiness.

Step 1: Review Your Insurance Policy Before a Storm Is Named

One of the biggest mistakes property owners make is waiting until a storm is approaching to look at their insurance policy.

By then, it may be too late to make changes.

Take time now to review:

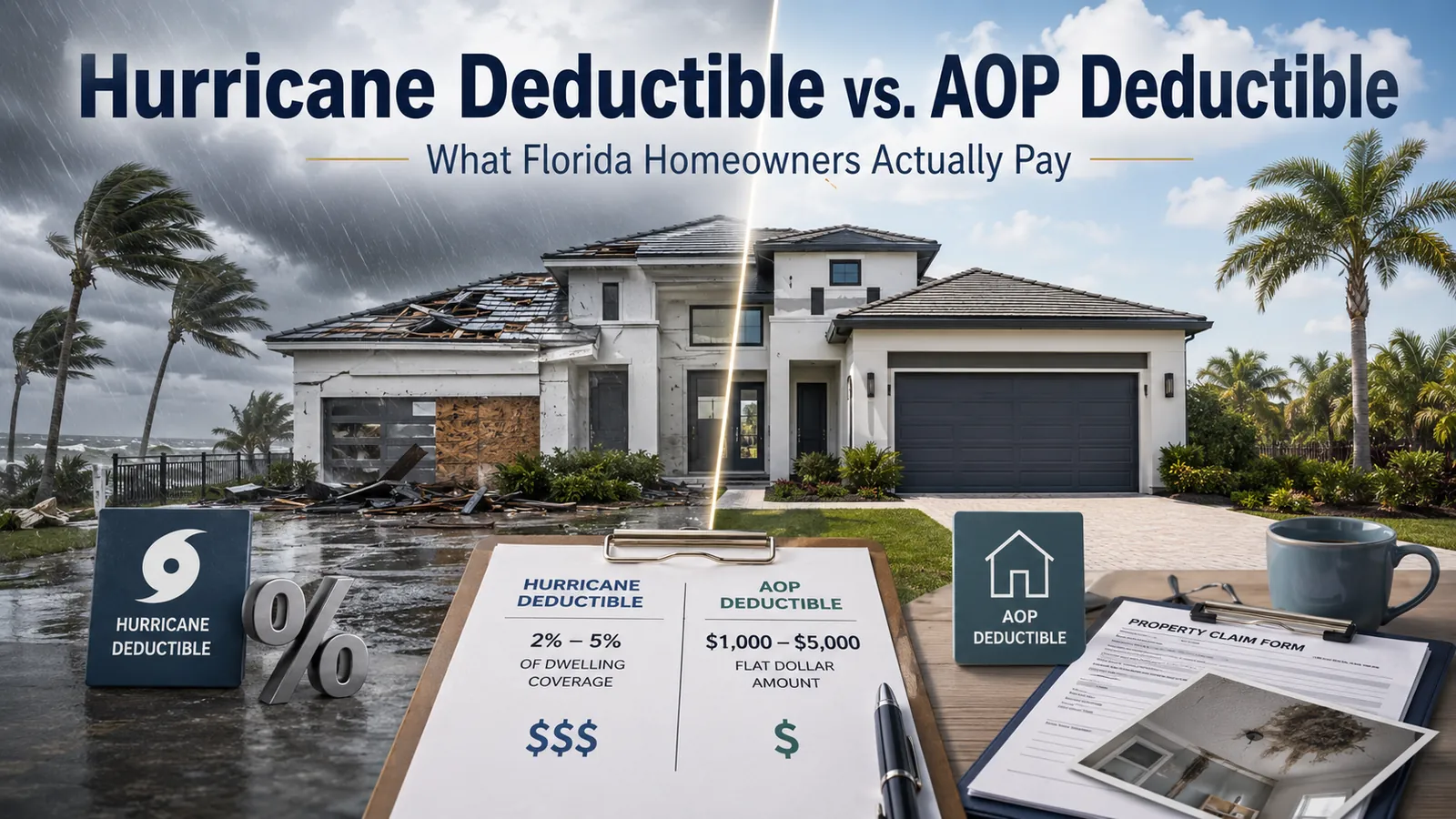

- Your hurricane deductible

- Your windstorm coverage

- Whether you have flood insurance

- Whether your policy covers replacement cost or actual cash value

- Any roof limitations or roof settlement endorsements

- Any water damage limitations

- Your duties after loss

- Deadlines for reporting damage

- Requirements for protecting the property from further damage

This is especially important in Florida, where hurricane deductibles, roof coverage limitations, and water damage exclusions can significantly affect what happens after a loss.

If you do not understand your policy, that is normal. Insurance policies are not written in plain English. But you should not wait until after a hurricane to find out what coverage you do or do not have.

For additional context on how insurers evaluate roof claims, you may also want to read our article on 6 common reasons roof claims are denied.

Step 2: Take Photos and Videos of Your Property Now

Pre-loss documentation can be extremely valuable in an insurance claim.

Before a storm is on the radar, take clear photos and videos of the condition of your property. This helps establish what your home or building looked like before the damage occurred.

Document the exterior, including:

- Roof slopes visible from the ground

- Gutters and downspouts

- Soffit and fascia

- Windows and doors

- Fencing

- Pool screens and enclosures

- Exterior walls

- Detached structures

- Landscaping near the home

- Any existing cracks, stains, or wear

Document the interior, including:

- Ceilings

- Walls

- Flooring

- Cabinets

- Closets

- Attic access areas

- Personal property

- Important electronics and appliances

For business owners, document inventory, equipment, signage, buildouts, tenant improvements, and any areas that would affect business operations.

You do not need professional photography. A smartphone is fine. The key is to capture the condition of the property before a loss occurs.

For a deeper guide on pre-loss documentation, read our related article: How to Document Your Home for Insurance BEFORE a Storm Hits.

Step 3: Keep Important Documents in a Safe Place

After a hurricane, access to documents can become a problem. Power may be out. Internet service may be down. Files may be damaged. You may be displaced from the property.

Create a digital folder with:

- Your insurance policy

- Declarations page

- Mortgage company information

- Photos and videos of the property

- Receipts for major repairs or upgrades

- Roof replacement records

- Plumbing, HVAC, or electrical records

- Prior inspection reports

- Contractor invoices

- Appraisals or property records

- Contact information for your insurance agent

- Emergency contractor contacts

Save copies in cloud storage and on a physical backup drive if possible.

You can also review FEMA’s general disaster planning guidance at Ready.gov and its hurricane-specific preparation guidance at Ready.gov Hurricanes.

Step 4: Walk Your Property Before the Storm

Before a hurricane or tropical storm approaches, inspect the property for conditions that could make damage worse.

Look for:

- Loose roof shingles or tiles

- Clogged gutters

- Weak tree limbs

- Damaged fencing

- Loose patio furniture

- Cracked windows

- Areas where water already ponds

- Signs of prior roof leaks

- Missing sealant around openings

- Debris around drains or scuppers

For commercial properties, inspect roof drains, parapet walls, rooftop equipment, signage, exterior lighting, and areas where water may collect.

If you find issues, address them before the storm. Insurance companies may scrutinize whether damages were caused by the storm or whether they existed beforehand.

Step 5: Understand the Difference Between Wind Damage and Flood Damage

This is one of the most important insurance issues in hurricane claims.

A standard property insurance policy may cover wind damage, but flood damage is typically separate. Storm surge, rising water, and flooding may not be covered unless you have a flood insurance policy.

That distinction can become a major issue after a hurricane, especially when a property has both wind damage and water intrusion.

Examples of potential wind-related damage may include:

- Roof covering damage

- Wind-created openings

- Broken windows from debris

- Interior water damage from storm-created openings

- Damage to exterior components caused by wind

Examples of potential flood-related damage may include:

- Rising water entering the structure

- Storm surge

- Overflow from bodies of water

- Groundwater entering the building

Because coverage can depend on the source of the water and the language in the policy, it is important to document everything carefully and avoid making assumptions about what is or is not covered.

If your property has roof damage, storm damage, or exterior damage, visit our Wind & Hail claims page. If you are dealing with interior water intrusion, you may also want to review our Water Damage claims page.

Step 6: Be Careful What You Sign After a Storm

After a major storm, contractors, mitigation companies, roofers, tree companies, and restoration vendors may show up quickly.

Some are reputable. Others may use high-pressure tactics.

Before signing anything, make sure you understand:

- What services are being authorized

- Whether pricing is clearly explained

- Whether you are assigning insurance benefits

- Whether the company is claiming the right to communicate with your insurer

- Whether there are cancellation rights

- Whether there are lien rights

- Whether you remain responsible for unpaid invoices

Emergency services may be necessary to protect the property, but you should still understand what you are signing.

Step 7: Report Damage Promptly, But Do Not Guess

If your property is damaged, report the claim promptly. At the same time, be careful not to guess about the full extent of damage before the property has been properly inspected.

After a hurricane, some damage is obvious. Other damage may not appear until days or weeks later.

For example:

- Roof damage may not be visible from the ground

- Water intrusion may appear after repeated rain

- Ceiling stains may develop over time

- Moisture can travel behind walls

- Tile, shingle, or metal roof damage may require a closer inspection

- Interior damage may worsen if mitigation is delayed

When reporting the claim, provide accurate information, but avoid minimizing the loss or making statements that could be misunderstood later.

Step 8: Keep a Claim Journal

Once a claim is opened, keep a record of everything.

Track:

- Date and time of the loss

- When you reported the claim

- Claim number

- Adjuster names and contact information

- Inspection dates

- Phone calls

- Emails

- Documents submitted

- Payments received

- Repair estimates

- Temporary repairs

- Additional damages discovered

This can be extremely helpful if the claim becomes delayed, underpaid, denied, or disputed.

Step 9: Do Not Assume the Insurance Company’s Estimate Is Complete

Insurance company estimates are not always complete. Sometimes they miss damaged areas. Sometimes they use pricing that does not reflect the actual cost of repair. Sometimes they include limited repairs when replacement may be required. Sometimes they fail to account for code upgrades, matching issues, overhead and profit, or interior damages.

This does not always mean the insurance company is acting in bad faith. But it does mean property owners should review the estimate carefully before assuming the payment is correct.

If the estimate seems too low, does not include all damaged areas, or does not match what contractors are telling you, it may be worth having the claim reviewed.

If your insurance company has already issued a low payment, visit our Underpaid Claims page. If the carrier denied the claim entirely, review our Denied Claims page and our article on how to dispute a denied homeowners insurance claim in Florida.

Step 10: Know When to Ask for Help

A hurricane claim can become complicated quickly.

You may want professional help if:

- Your claim is denied

- Your payment seems too low

- The insurer says the damage is wear and tear

- The insurer says the damage is not storm-related

- The estimate does not include all damaged areas

- There are delays in the claim

- The insurer requests repeated inspections

- You are being asked for documents you do not understand

- There is a dispute over roof damage, water damage, or cause of loss

- You own a commercial property or rental property with significant damage

A licensed public adjuster represents the policyholder in the insurance claim process. That means the public adjuster reviews the damage, evaluates the policy, prepares and supports the claim, communicates with the insurance company, and works to help the property owner pursue the benefits available under the policy.

To learn more about what a public adjuster does and when it may make sense to hire one, read our article: Should I Hire a Public Adjuster or Handle My Insurance Claim Myself?.

The Bottom Line

Hurricane season starts today. The time to prepare is now.

Do not wait until a storm is approaching. Do not wait until your roof is leaking. Do not wait until the insurance company has already inspected the property and issued a payment that does not come close to the actual repair cost.

Take photos. Review your policy. Save your documents. Prepare your property. Understand your coverage. Know who to call if damage occurs.

At NeJame Claims Adjusting, we help Florida homeowners and business owners navigate the insurance claim process after hurricanes, windstorms, water losses, and other property damage events.

Need Help With a Hurricane Damage Claim?

NeJame Claims Adjusting represents policyholders, not insurance companies.

If you have hurricane, wind, roof, or water damage, contact our team before accepting a settlement that may not fully address your damages.

Contact NeJame Claims Adjusting today or call 407-637-1000 for help reviewing your property damage claim.