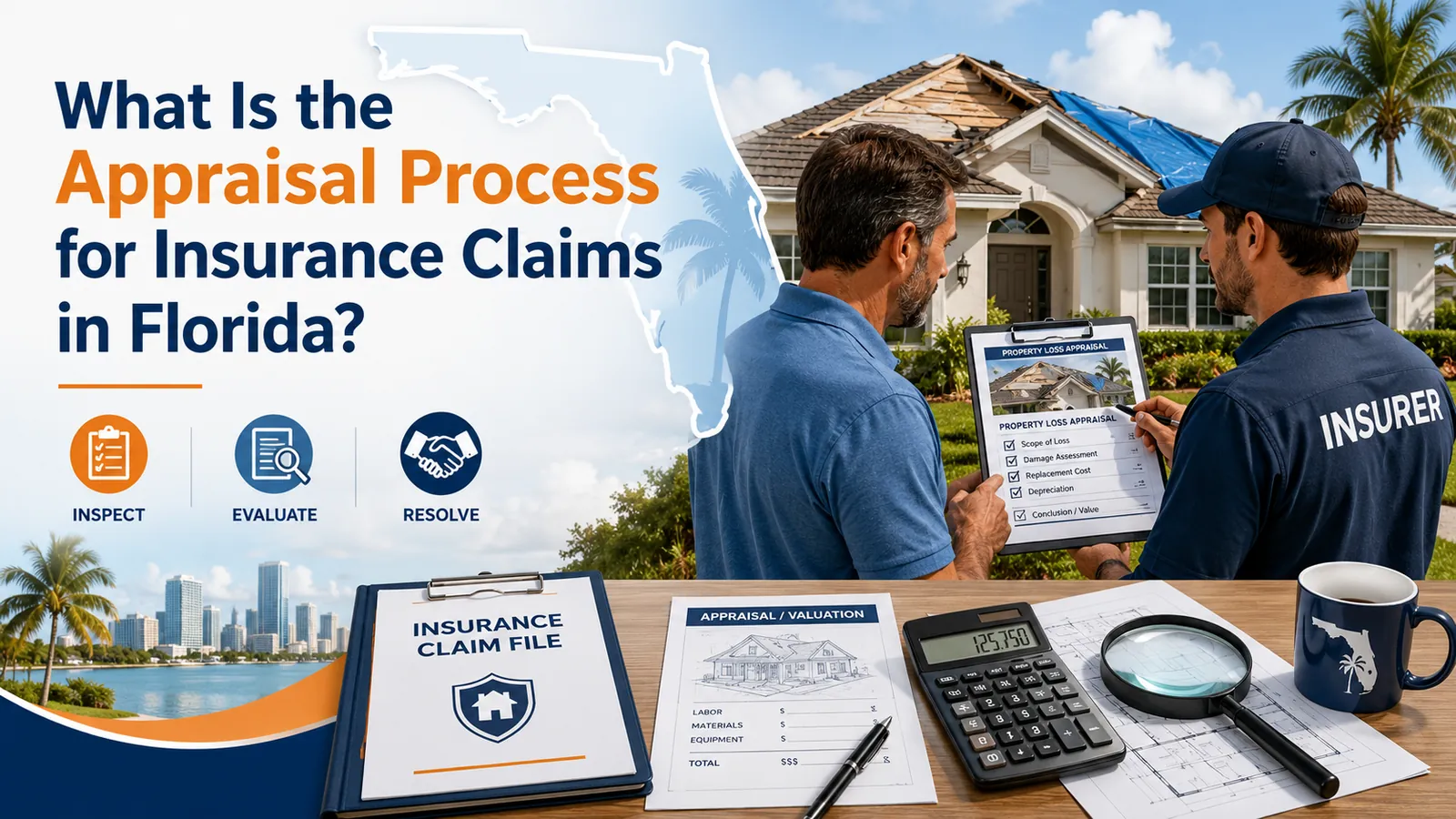

What Is the Appraisal Process for Insurance Claims in Florida?

The insurance appraisal process in Florida is a binding dispute resolution method used when you and your insurance company disagree on how much your property damage claim is worth — not whether it's covered. Each side selects an independent appraiser, the two appraisers try to agree on the value of the loss, and if they can't, a neutral umpire makes the final decision. The appraisal clause is found in most Florida homeowners insurance policies, typically in the "Conditions" section, and either party can invoke it by sending a written demand.

That's the short version. But the appraisal process has nuances that can make or break its effectiveness for your claim — from knowing when appraisal is the right tool to choosing the right appraiser to represent your interests. This guide covers the full process from a public adjuster's perspective, with a focus on what Central Florida homeowners actually need to know.

Appraisal vs. Real Estate Appraisal: They Are Not the Same Thing

This is the most common point of confusion. When most people hear "appraisal," they think of the process a bank uses to determine their home's market value before approving a mortgage. An insurance appraisal is something entirely different.

An insurance appraisal determines the cost to repair or replace property damage after a covered loss. It has nothing to do with what your home is worth on the real estate market. The question being answered is specific: how much money does it take to restore your property to its pre-loss condition? That figure is based on construction costs, material pricing, labor rates, and the scope of work required — not comparable home sales or neighborhood trends.

This distinction matters because the appraiser you choose needs construction and insurance expertise, not real estate credentials. The best appraisers for this process are licensed public adjusters, experienced contractors, or engineers who understand how to scope damage, price repairs using industry-standard estimating tools like Xactimate, and present findings in a format that holds up against the carrier's own documentation.

How the Appraisal Process Works Step by Step

The appraisal process follows a consistent framework, though the specific language varies slightly from policy to policy. Here's how it typically unfolds.

Invoking the clause. Either you or the insurance company can demand an appraisal by sending a formal written request to the other party. Most policies require this to be done in writing. Once invoked, both sides are obligated to participate according to the terms of the policy. Before you invoke appraisal, make sure you've reviewed your policy's specific appraisal language — some policies require both parties to agree, while others allow either side to demand it unilaterally.

Selecting appraisers. Each party selects one independent, competent appraiser within 20 days of the written demand (the exact timeframe depends on your policy language). You choose yours, and the insurance company chooses theirs. Your appraiser is your advocate in this process — they will inspect the property, prepare a detailed estimate of the loss, and negotiate with the carrier's appraiser to reach agreement on the value of the damage.

Choosing an umpire. The two appraisers then select a neutral umpire. If they can't agree on an umpire within 15 days (again, check your specific policy), either party can petition a court to appoint one. The umpire serves as the tiebreaker if the two appraisers can't reach full agreement.

Reaching an award. The appraisers independently inspect the property, prepare their own estimates, exchange reports, and attempt to agree on the total amount of loss. If they reach full agreement, that figure becomes the binding appraisal award. If they agree on some items but not others, the disputed items go to the umpire. A decision agreed to by any two of the three panel members — either both appraisers, or one appraiser and the umpire — sets the final amount. That award is binding on both you and the insurance company.

When Appraisal Is the Right Tool

Appraisal is powerful, but it's not always the right path. Understanding when it works — and when it doesn't — can save you time, money, and frustration.

Appraisal works when the dispute is about money, not coverage. If your insurance company acknowledged that your damage is covered but offered a settlement that doesn't come close to the actual repair cost, appraisal is designed exactly for this situation. This is extremely common with roof damage claims in Central Florida, where carriers frequently approve a claim but undervalue the scope of work. Our post on the 25 percent rule for roofs explains one of the most common areas where carriers and contractors disagree on scope. Orange Contracting and Roofing's analysis of why Florida roof insurance payouts fall short goes deeper into the specific line items carriers regularly underestimate.

Appraisal does not work when the carrier denied your claim entirely. If the insurance company says the damage isn't covered at all — claiming it's excluded, pre-existing, or not caused by a covered peril — appraisal can't help. There's no "amount of loss" to dispute when the carrier's position is that they owe you nothing. Florida courts have consistently ruled that a complete denial of coverage takes the dispute outside the scope of appraisal. In that scenario, mediation or litigation is the appropriate path. Our guide on how to dispute a denied homeowners insurance claim in Florida walks through all available options.

Appraisal can also work after you've already received a partial payment. Many homeowners don't realize this. Accepting a check from your insurance company does not mean your claim is settled or closed. If you received a payment that falls short of what repairs actually cost, you can still invoke appraisal to pursue the difference.

What Appraisal Costs and Who Pays

Unlike state-administered mediation, which is free to the homeowner, appraisal does come with costs. Understanding the financial structure upfront helps you decide whether it makes sense for your claim.

Each party pays for their own appraiser. That means you're responsible for the fee of the appraiser you select. The cost of the umpire, if one is needed, is split equally between you and the insurance company. Additional costs may include site inspections and detailed estimate preparation by your appraiser.

Your appraiser's fee varies depending on the complexity of the claim. Some appraisers charge a flat fee, while others work on a contingency basis (a percentage of the increase over what the carrier originally offered). For larger claims involving extensive roof, water, or structural damage, the resulting increase in the award typically far exceeds the cost of the appraiser's fee.

The key financial question is simple: is the gap between what the carrier offered and what the repairs actually cost large enough to justify the expense? For a $5,000 difference on a straightforward claim, the math may not work. For a $30,000 or $50,000 gap on a roof replacement or multi-system loss, appraisal almost always pays for itself.

The Relationship Between Mediation and Appraisal

Florida law creates a specific sequence between mediation and appraisal that many homeowners — and even some professionals — don't fully understand.

Under Florida Statute §627.7015, insurance companies are required to notify homeowners of their right to participate in the state-administered mediation program before demanding appraisal. This notification must happen at the time a claim is filed. If the carrier fails to provide this notice, they may waive their right to compel appraisal.

From a practical standpoint, mediation is designed as a pre-appraisal step. It's non-binding, free to the homeowner, and often resolves disputes without the cost and formality of appraisal. If mediation doesn't produce a satisfactory result, you can then move to appraisal (assuming your policy contains the clause). The two processes serve different purposes: mediation is a facilitated negotiation; appraisal is a binding valuation determination by a panel of experts.

One important strategic consideration: if you invoke appraisal first without attempting mediation, you may be bypassing a free opportunity to resolve the claim. Conversely, if the carrier invokes appraisal prematurely — before conducting a thorough investigation — that can be a tactic to limit your recovery. Consulting with a public adjuster before committing to either path is generally the smartest approach.

How to Choose the Right Appraiser

Your choice of appraiser is arguably the most important decision you'll make in the entire process. The appraiser you select will inspect your property, prepare the estimate that forms the basis of your position, and negotiate directly with the carrier's appraiser to reach agreement.

Look for construction and insurance expertise. The ideal appraiser understands both how repairs are scoped and priced and how insurance policies work. Licensed public adjusters with construction backgrounds are particularly well-suited for this role because they speak both languages — they can prepare estimates in Xactimate (the industry-standard software used by most carriers), identify damage the carrier's adjuster may have missed, and present their findings in a format the carrier's appraiser has to engage with substantively.

Avoid appraisers without property damage experience. A real estate appraiser, a general home inspector, or someone without direct experience in insurance claim valuation is not the right choice, regardless of their credentials in other areas. Insurance appraisal is a specialized process that requires specialized knowledge.

Ask about their track record with your type of claim. An appraiser who primarily handles commercial claims may not be the best fit for a residential roof loss, and vice versa. Ask specifically about their experience with your claim type and the carrier you're dealing with.

At NeJame Claims Adjusting, we serve as appraisers for homeowners across Central Florida. Our founder's background as both a former carrier-side staff adjuster and a licensed general contractor gives us a unique advantage in the appraisal process — we understand how carriers build their estimates, where they commonly miss damage, and how to prepare documentation that maximizes the award. We work closely with Orange Contracting and Roofing to ensure that the construction scope presented in appraisal reflects actual repair costs, not theoretical numbers.

When Appraisal Can Be Waived

The right to appraisal isn't absolute. There are several circumstances under which it can be waived by either party.

If the insurance company fails to notify you of your right to mediation as required by Florida Statute §627.7015, the carrier may waive its right to demand appraisal. If either party files a lawsuit, that action can waive the right to appraisal depending on the circumstances. Some policies have strict deadlines for when appraisal must be requested — missing those deadlines may eliminate the option. And some Florida carriers have removed the appraisal clause from their policies entirely. If your policy doesn't contain one, appraisal isn't available regardless of the circumstances.

Before assuming appraisal is an option, read your policy carefully and consult with a public adjuster or attorney who can assess your specific situation.

Frequently Asked Questions

Is an insurance appraisal award final? Yes. Appraisal awards are binding on both parties. Once an award is signed by any two members of the three-person panel (both appraisers, or one appraiser and the umpire), it sets the amount of loss. Overturning an appraisal award in court is extremely difficult and generally requires proving fraud or collusion among panel members.

Can the insurance company force me into appraisal? It depends on your policy language. Most Florida homeowners policies allow either party to demand appraisal, which obligates the other side to participate. However, if the carrier failed to offer mediation first as required by law, or if they denied your claim entirely, their right to compel appraisal may be waived.

Can I use appraisal if my claim was denied? Generally, no. Appraisal resolves disputes about the dollar amount of a loss, not whether the loss is covered. If your carrier denied coverage entirely, you'll need to pursue mediation or litigation to address the coverage question first. If the carrier acknowledged partial coverage but you disagree with the amount, appraisal can address the valuation dispute.

How long does the appraisal process take? Timelines vary, but most residential appraisals in Florida are completed within 30 to 90 days from the date appraisal is invoked. Complex claims with significant damage or disputes over umpire selection can take longer. Your appraiser can give you a realistic timeline based on your specific claim.

Can a public adjuster serve as my appraiser? Yes, and they're often the best choice. Public adjusters are licensed insurance professionals with direct experience in damage assessment, scope preparation, and claims negotiation. A public adjuster who also has construction knowledge can provide the most comprehensive representation in the appraisal process.

The Bottom Line

The appraisal process is one of the most effective tools Florida homeowners have for resolving underpaid insurance claims without going to court. When the dispute is about how much the carrier owes — not whether they owe anything — appraisal puts the valuation question in the hands of qualified experts rather than leaving it to the carrier's own adjuster.

The keys to a successful appraisal are knowing when it's the right tool, choosing the right appraiser, and having thorough documentation of the damage and repair costs. At NeJame Claims Adjusting, we guide Central Florida homeowners through every stage of this process — from the initial policy review to serving as their appraiser and negotiating the final award. Contact us for a free claim assessment to find out whether appraisal is the right path for your situation.